We don't know why Malawi is poor

And that’s a problem for forecasting economic growth

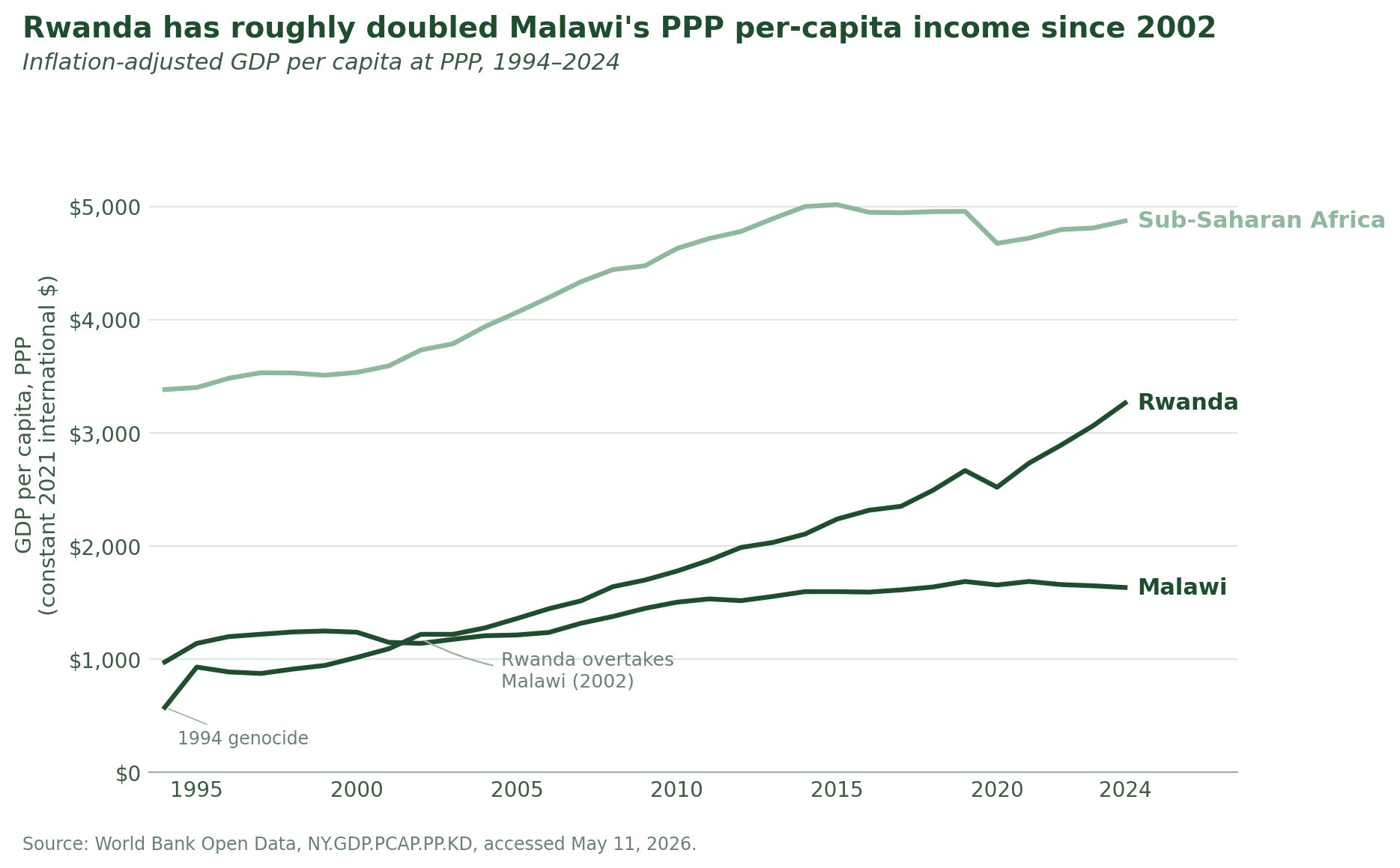

In 1994, Rwanda’s GDP per capita was $5751. The country had just emerged from a genocide that killed roughly 800,000 people in 100 days, which amounts to about 11% of the population. The educated class had been murdered or fled, infrastructure was destroyed, and the state had collapsed.

Malawi in 1994 was poor too, but functioning. Hastings Banda’s three-decade dictatorship had just ended in a peaceful democratic transition. With a GDP per capita of $976, roughly 70% higher than Rwanda’s, Malawi was meaningfully better off than post-genocide Rwanda by any reasonable measure.

Thirty years later, Rwanda’s GDP per capita is $3,265. This is nearly six times higher than its 1994 trough, and roughly twice Malawi’s $1,634. Rwanda's GDP per capita has grown by about 4.5% per year in real terms over the past decade, but Malawi's has fallen for three consecutive years.

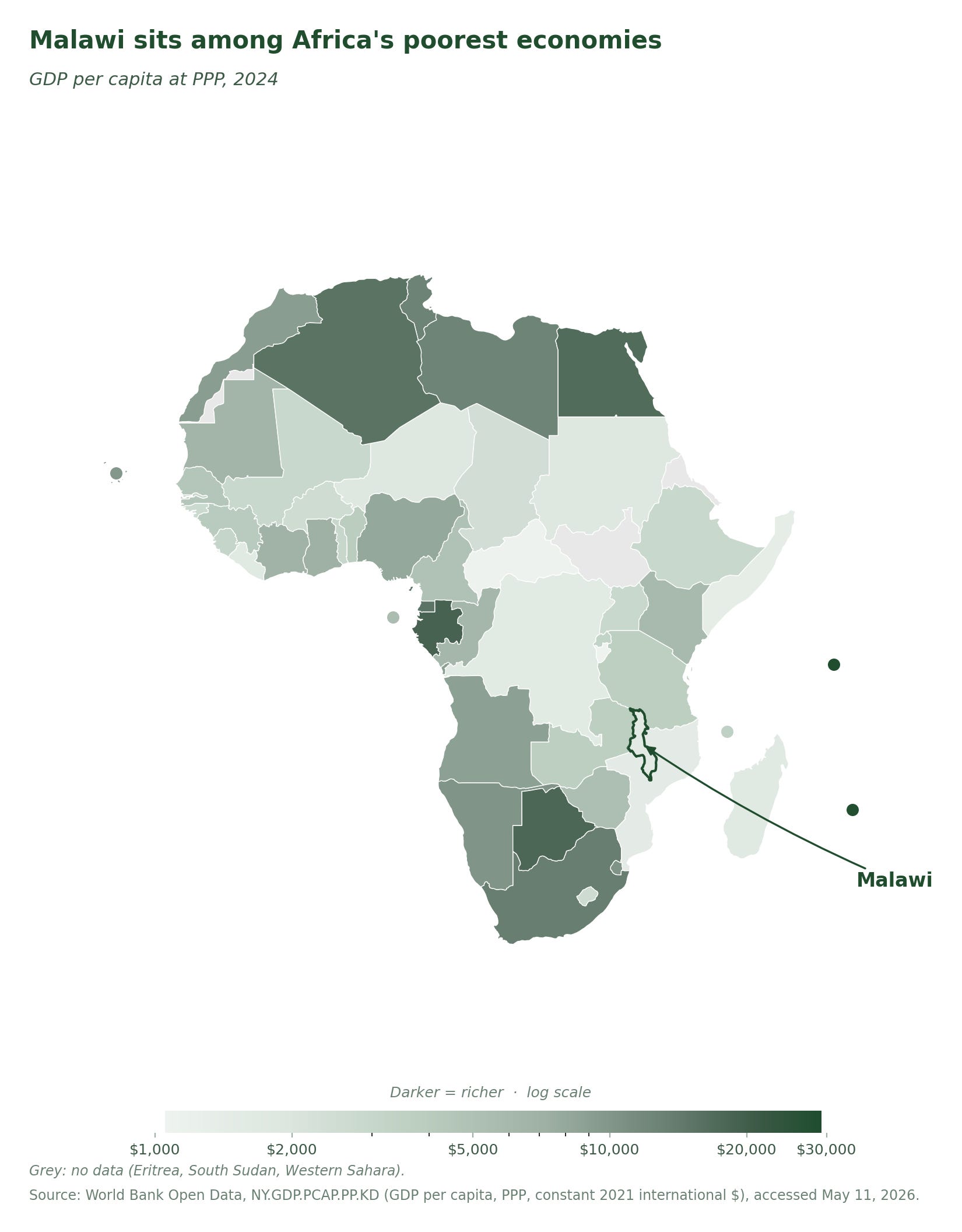

The rest of the East African comparison group has pulled away too. Kenya’s GDP per capita is roughly $5,800, over three and a half times Malawi's. The sub-Saharan African average is $4,873, also nearly three times. Even within a region full of poor countries, Malawi is unusual.

A few headline numbers:

The World Bank ranks Malawi among the ten poorest countries in the world by GDP per capita at PPP.

70% of Malawians live on less than $2.15 a day. Under the World Bank’s revised $3-a-day poverty line, it’s 75%.

Malawi is home to 0.24% of the world’s population but roughly 2% of the world’s extreme poor.

GDP per capita has fallen for three consecutive years (2022–2024). Population growth of 2.6% per year is now outrunning real economic growth.

Roughly 80% of the population works in agriculture, mostly on rain-fed maize plots. About 76% of farms are smaller than one hectare.

Around 15% of the population has access to electricity.

Lots of countries are poor, though. The interesting bit is, we don’t really have a great answer as to why Malawi is.

For many of the world’s poorest countries, there’s some obvious issue that is pointed to. Regional or civil war, state collapse, ongoing ethnic conflict, coups, jihadist insurgencies… the list is quite long.

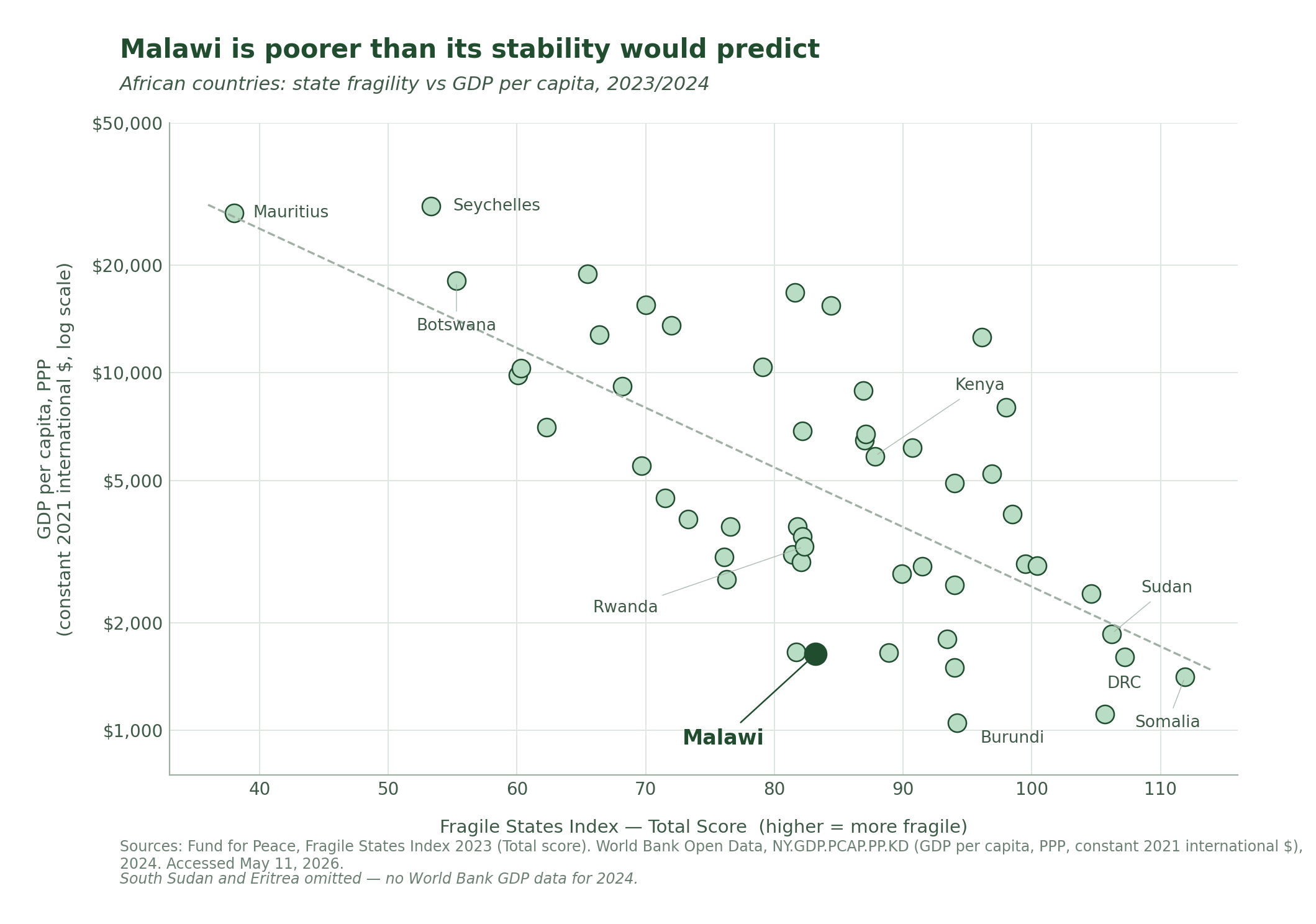

But Malawi has been at peace for its entire post-independence history. It has held competitive multiparty elections every five years since 1994 and has experienced peaceful transfers of power across parties. It has no significant ethnic conflict, no separatist movement, no insurgency. It was not a victim of the resource curse, and it has not had a recent mass atrocity. It ranks 107th out of 180 on Transparency International’s Corruption Perceptions Index, which is middling, but not especially bad, roughly comparable to Indonesia and Brazil.

Malawi has also long been a darling of donors. Malawi’s aid per capita in 2023 was roughly 2.5x the global average. It is also a member in good standing of SADC, the African Union, and the Commonwealth, on no major sanctions list. There is no equivalent of Eritrea’s seclusion, Zimbabwe’s pariah status under Mugabe, or Sudan’s international isolation.

Donor spending in Malawi is dominated by health, especially HIV/AIDS. The rest goes mostly to agriculture, education, and the Social Cash Transfer Program. The health spending has helped: HIV positivity fell from around 14% to 7% over the PEPFAR era. The rest is weaker in impact, though why would merit its own full post.

This is where some readers might object that we do know why Malawi is poor! After all:

Agricultural productivity is very low. Around 80% of the population works the land, mostly on rain-fed maize plots smaller than one hectare. Yields per hectare are well below regional potential. Output per agricultural worker is among the lowest in the world.

There is almost no manufacturing. Manufacturing contributes around 10% of GDP, and most of that is food processing, beverages, and cigarettes for the domestic market. No garments, no electronics assembly, no meaningful light-manufacturing-for-export.

Human capital is thin. Mean years of schooling sit around 5. Stunting rates have been at 35-40% for decades, with measurable downstream effects on adult cognition and earnings.

Infrastructure is bad. Around 15% of the country has electricity. Internal roads are rough. Internet penetration is among the lowest globally.

Exports are concentrated in declining commodities. Tobacco accounts for roughly half of merchandise exports, and global demand for tobacco has been falling for decades.

This is all true and well-documented. It is also, upon reflection, mostly a description of being poor rather than an explanation. “Malawi is poor because its agricultural productivity is low” is closer to a tautology than an answer.

There are certainly some candidate theories, and they make sense, but none seem to really be fully explanatory.

Institutions. Acemoglu and Robinson’s Why Nations Fail argues poor countries are stuck with extractive institutions inherited from colonial rule, while rich countries developed inclusive ones that protect property rights and constrain elites. But Malawi’s institutions are imperfect but functional, with a multiparty democracy, peaceful transfers, and working courts, and broadly better than Rwanda’s (executive concentration, restrictions on political opposition), Vietnam’s (one-party state, no political competition), or China’s. This might explain why Malawi is not rich but does not seem to satisfy why it is so poor, even by low-income country standards.

Geography. Jeffrey Sachs and others have long argued that geography is destiny: landlocked, tropical, distant-from-markets countries face structural penalties through transport costs, disease burden, and weak agricultural conditions. Malawi has all three. Sure, but the empirical literature pegs the landlocked penalty at about 1% of annual growth. This is meaningful over decades, not enough to close a gap this large in per-capita income. Rwanda is more landlocked than Malawi and has grown faster. Uzbekistan is double-landlocked and has roughly tripled per-capita income since 2000.

Colonial history. This is a more specific version of the institutions story: that the type of colonial inheritance matters more than the fact of colonialism itself. Settler colonies (Kenya, Zimbabwe) got infrastructure and an agrarian capitalist class; labor-reserve colonies got nothing but a system for exporting workers. Malawi was the latter, administered as a labor reserve for South African and Rhodesian mines, with minimal investment in roads or schools. At independence in 1964 there were something like 30 university graduates in the country. But Botswana’s colonial inheritance was just as thin (a British protectorate run on a shoestring), and South Korea emerged from brutal Japanese occupation followed by a war that destroyed most of the country. Initial conditions matter, but they clearly don’t determine the outcome, particularly once enough time has passed, and especially given the funding and effort that has gone toward changing those initial conditions by donors since then.

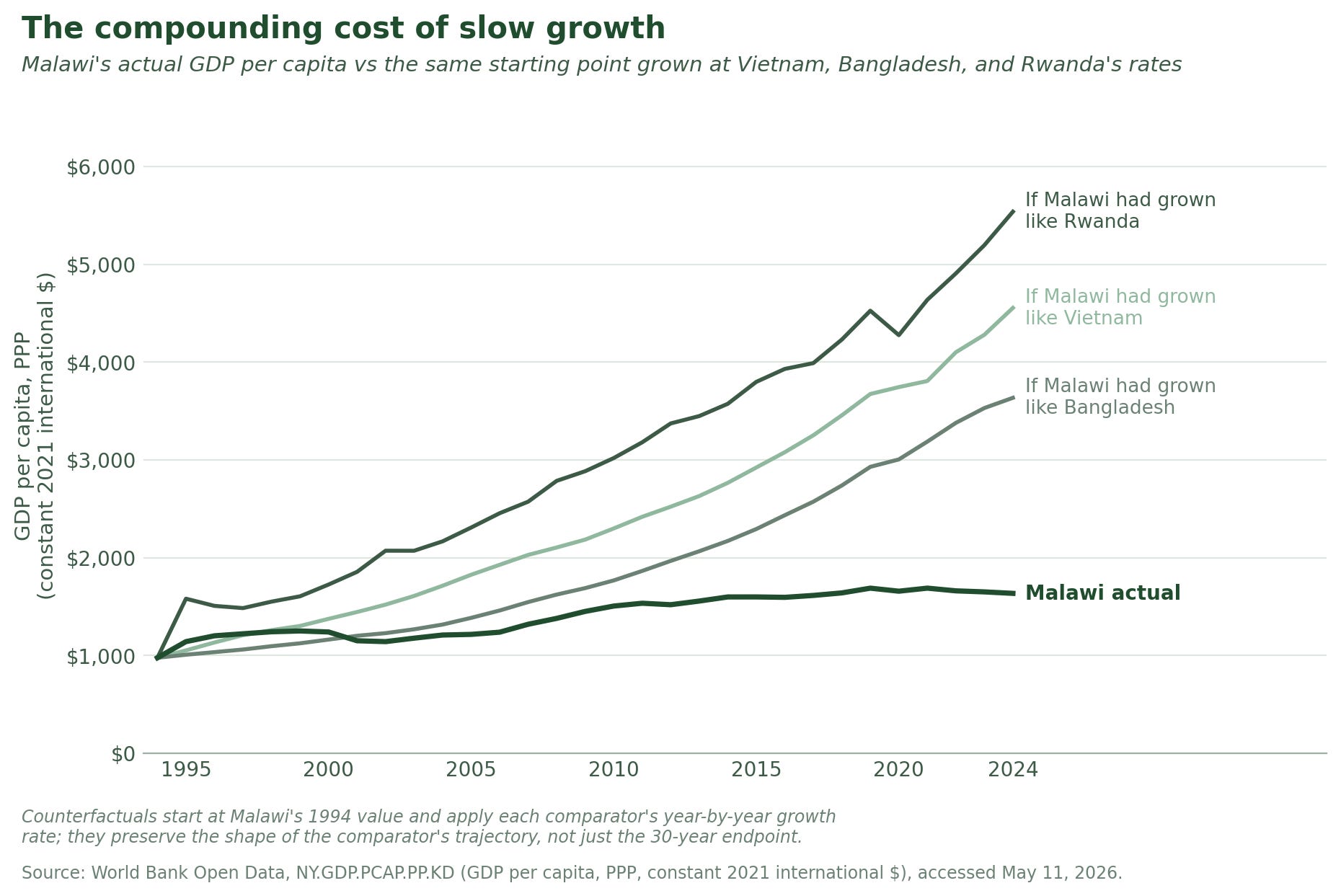

Trade and industrial policy. Dani Rodrik and others argue that escape from poverty in the modern era runs through plugging into global value chains, things like apparel, electronics assembly, light manufacturing, that absorb underemployed rural workers at productivity levels above subsistence farming. Vietnam, Bangladesh, Cambodia, and Ethiopia all did this. Even Lesotho, a small landlocked southern African country with a similarly agrarian profile to Malawi, built a textile industry employing tens of thousands through AGOA preferences, and is now more than 1.5x as rich per capita. Whether Malawi missing out was a policy failure (no industrial strategy, no SEZs that worked, an overvalued currency for long stretches) or a fundamentals problem (transport costs, scale, electricity reliability) is contested. Both are probably true.

Agroecology. The crops a country can grow at scale matter more than economists usually let on. Some agroecologies offer high-value tradable cash crops (coffee, cocoa, palm oil, cut flowers). Malawi’s cards are unusually weak: maize is low-value and politically locked in by food-security policy, and tobacco — long the main cash export — is in secular global decline. Compared to Ethiopia (coffee), Kenya (tea, horticulture), Rwanda (coffee, tea), Côte d’Ivoire (cocoa), Vietnam (rice and coffee for export). But Bangladesh had no high-value cash crops either and built a garment industry that pulled tens of millions out of poverty. A weak agricultural hand constrains the menu of options but doesn’t determine the outcome.

Political settlements. The political-settlements view — associated with Stefan Dercon’s Gambling on Development — argues that countries grow when their elites strike a credible bargain to pursue growth rather than divide the existing pie. Botswana’s diamond-era settlement under the BDP, Rwanda’s post-genocide bargain under the RPF, China under Deng, and Ethiopia under Meles are the canonical cases. Since 1994, multiparty politics has been organized around a median voter who is a smallholder maize farmer, and no political faction has committed credibly to a transformation agenda that imposes short-term costs on this constituency. The result is a stable equilibrium, visible in three concrete places:

The fertilizer subsidy program (FISP) consumes up to three-fourths the agriculture budget in some years to subsidize maize inputs for smallholders. It is politically untouchable because rural maize farmers are the median voter. Several administrations have made some attempt to reform it and backed down. Resources that could go to roads, irrigation, or diversification go to propping up the existing structure.

Maize self-sufficiency policy (periodic export bans, price controls, the elevation of maize availability over agricultural commercialization) caps farmer returns and discourages the shift into higher-value crops. While Vietnam leaned into rice exports and used the proceeds to industrialize, Malawi has done the opposite.

Land tenure is mostly customary, administered by chiefs. You can’t easily mortgage farmland, sell it to a more productive farmer, or aggregate plots into commercial units. Plots subdivide across generations and everyone stays a subsistence farmer on less land. Reform attempts have stalled because chiefs lose power.

Why some countries get this bargain and others don’t is contingent and historical, not predictable in any deep way. Since we can’t really name why one country settles on a good political bargain and others don’t, it has limited ability to explain why this is what happened. This is describing a bad equilibrium but not explaining how it came to be and how to avoid or get out of one.

It’s tempting to say that no single theory explains Malawi but the combination does. The problem is that the same combination applies to countries that escaped. Bangladesh had a thin colonial inheritance, a weak crop hand, and chronic political dysfunction, and grew a manufacturing industry anyway. Rwanda is more landlocked than Malawi, had its human capital base annihilated in 1994, and grew anyway. Vietnam was bombed and ran a command economy into the ground before its takeoff. If you’d lined these countries up in 1990 and asked which would be in the bottom five globally by 2024, Malawi would not have been an obvious pick on the factors named above.

The fact that we don’t have a particularly good explanation matters for more than just Malawi. Development economics has been bad at predicting which poor countries will grow, by how much, and why for as long as the field has existed. The East Asian miracle wasn’t expected; in the 1960s, the World Bank was more bullish on Burma and the Philippines than on South Korea. This is also true of the African growth boom of the 2000s, which was dismissed as a commodity blip when it began. Same with Vietnam’s takeoff, Rwanda’s, and Botswana’s. Nor were the failures: Argentina’s century-long decline, Venezuela’s collapse, the post-Soviet stagnation outside the Baltics, or India’s stagnation under license raj.

Every proximate factor named (institutions, geography, colonial inheritance, missed trade windows, weak crop hand, distributive political settlement…) doesn’t predict outcomes nor do they seem to satisfyingly capture much of the reason for variation. You might object that explanation doesn’t require prediction, but development economics specifically exists to tell countries what to do. An explanatory toolkit that can’t generate ex ante predictions about which countries with which interventions are likely to take off isn’t doing that. We are sense-making after the fact.

So what does this mean?

Don’t treat proximate factors as explanations. "Malawi is poor because of low agricultural productivity / weak institutions / bad geography" is mostly just restating the outcome. Development writing, including in serious outlets, does this often, and it forecloses the actual question of why these conditions persist in this country and not its neighbors.

The unit of analysis for "why is X poor" may be the political coalition, not the country. Malawi's story becomes legible once you ask whose interests policies serve: smallholder maize farmers as median voter, chiefs controlling customary tenure, FISP as the price of rural votes. This is also why aid targeted at health outcomes has succeeded dramatically in places like Malawi while aid targeted at growth has not: health interventions can largely work around the political settlement, while growth interventions have to move through it.

Be skeptical of AI-and-growth forecasts that don’t name a mechanism for getting past the political settlement. We’ve made enormous strides in agricultural technology. Malawi has seen increases in agricultural productivity, but not as much as the technology alone would predict, and those it did see were swallowed into the same smallholder farmer equilibrium rather than disrupting it. Yes, AI may further things like, say, agricultural productivity, but if Malawi has not capitalized fully on historical gains due to political settlements so far, there needs to be reason to believe new tech will be different. This isn’t an argument that AI won’t matter for LMIC growth, but it’s a note that - in order to believe AI will matter in a particular way - you must first figure out what impact historical technological advances have had and why.

GDP per capita values in this article are in constant 2021 international dollars at purchasing power parity (PPP). This basis adjusts for both price-level differences between countries and inflation over time. Source: World Bank Open Data, indicator NY.GDP.PCAP.PP.KD, accessed May 11, 2026.

I doubt it's a huge contributing factor, but one interesting thing is that under Banda they co-operated with apartheid South Africa, the only Black African country to do. From what some of my Malawian colleagues have told me, there is still much lingering resentment about this which makes deals with neighbours sometimes politically difficult, which is a huge factor for a mountainous and landlocked country.

That said my own perception is that Malawi has fallen into a weird democracy trap where it's just democratic enough that short-term solutions win elections - there's currently a massive road building project in Lilongwe and there's the agricultural policies you mentioned - but there's no ability to invest in longer-term projects, AND simultaneously the short-term fixes don't really work and either balloon in cost or don't get maintained.

One question for me, having been to many African countries, is that Malawi just doesn't _feel_ as poor as some others, despite being statistically richer. Maybe it's the stability and safety but Malawi is sandiwched between Eritrea and Somalia, and having been to both Malawi feels like it's in a league above! It feels better than Burkina Faso, which ostensibly has double the GDP. But that's just anecdote.

It's an interesting question, one that should occupy more of more people's mindshare. Here are a number of thoughts that could be useful for you to consider:

1. I don't think Malawi is a special puzzle and other poor countries are not. Very few poor countries have monocausal development stories. War and state collapse explain short-term shocks, but many countries have overcome those to grow--as a result of many other factors.

The article itself lists multiple candidate explanations for Malawi, so I was confused as to why you tried to frame Malawi as a mystery. The fact that no single factor fully explains Malawi's outcome does not mean we lack explanations. Multicausal accounts are still explanations--just more complex ones that people far too often claim are "unsatisfying". (The development process isn't intended to "satisfy" anyone.)

A better framing could be around the residual--many of the factors listed in the article do go some ways in explaining Malawi's economic development level, but perhaps not all of it. It almost seemed like that "unexplained portion" is what you were after in the article, but you never said it explicitly.

2. I'm not a fan of the "tautology" critique. Development is fundamentally a complex process characterized by deep endogeneity and all manner of feedback loops that are hard to pin down. The factors you mention--ag productivity, lack of structural transformation, low human capital, etc.--are simultaneously outcomes of and inputs to economic development. This is the case in Malawi just like anywhere else.

Yes, one can and should dig deeper, but articulating these factors is itself useful because many of these things are both causes AND levers...the latter of which is important for policy.

3. The article frames institutions, geography, and colonial history as "proximate" — but the standard development literature treats these as deep causes of long-run income differences. See the diagram here from Rodrik and Subramanian's famous paper:

https://www.researchgate.net/figure/The-three-deep-determinants-of-income-by-Rodrik_fig1_325342409

Geography is hard to change, and institutions move slowly. The article's claim that these factors "don't predict outcomes nor satisfyingly capture much of the reason for variation" conflates two distinct questions: explaining levels of development and explaining changes in growth rates. Much of the institutions literature is explicitly trying to explain long-run income levels, not short-to-medium-run growth accelerations.

This matters because post-WWII growth in developing countries has been episodic — punctuated accelerations and decelerations — whereas growth in Western economies over the preceding century was more steady despite major disruptions. Slow-moving structural factors like institutions and geography are unlikely to explain these episodes on their own.

The interaction between slow and fast-moving factors (e.g., political dynamics, policy) probably matters a lot, and the article misses this.

4. The article states that Malawi's institutions are "broadly better than Rwanda's, Vietnam's, and China's." This is a claim that few if any development professionals would make, and it is almost certainly wrong. (I'd be surprised if this were true in the relatively poor quant measures we have of political institutions, and knowing friends who have worked in these places and having worked on some and been in all of them myself, I don't know anyone who would make such a claim.)

The institutions literature focuses as much on economic institutions as political ones--which you don't mention. We shouldn't necessarily equate formal democratic procedures — competitive elections, peaceful transfers — with institutional quality writ large (or even with genuinely inclusive political institutions, for that matter). Malawi may score reasonably on electoral competition while having weak economic institutions, which aligns with the political economy points around agriculture and land.

5. I'm not an ag or agronomy expert, but I do know through my own work that Malawi does in fact have some meaningful ag opportunities--in soya, sorghum, mangoes, and macadamia nuts, among others. The failure to capitalize on these opportunities points back to policy choices, political economy constraints, and the other structural factors listed elsewhere in the article

6. I've come to believe in the power of political economy explanations, which the article rightfully emphasizes. There is more literature out there that would help to unpack the emergence of the political settlement you mention.

More broadly, you mention political economy in the end as an important takeaway, after having framed it as describing an equilibrium rather explaining why it exists. Well, that sounds like a call to dig deeper on the political and economic history...not a reason to brush it off.

7. The claim that "development economics specifically exists to tell countries what to do" is not an accurate or widely shared definition of the field. Many development economists would not describe their work this way, and the field has a substantial body of work oriented toward understanding causes rather than prescribing action. This is why people like me and my colleagues, and people like Ken Opalo, make the distinction between academic research and policy research.

I think this points to a fundamental confusion between causes and levers. The causes of a country's development level and the available levers for changing it are separate problems. Geography may be a deep cause but is largely not a directly actionable lever — though transport infrastructure and trade integration offer partial handles. Trade and industrial policy are more tractable levers but may not be root causes.

The article opens by asking about causes and closes by criticizing development economics for failing to generate prescriptions. Those are different concerns, and conflating them doesn't actually get us much closer to answering the relevant policy questions.